A couple of days ago I wrote about a new collective consciousness to saving us on this planet (my 2017 review), a new level of enlightenment by many that find a higher level of connectedness due to the arising awareness of the need for a Green, Inclusive and Open Economy. We all know our life conditions shape our level of consciousness, and this year in particular has been hopeful, too many prompters show the need for a new world order embracing this new paradigm. And more and more friends show up to make it happen.

Today I want to write about the ‘dark side’. For a year now we have to witness the decay and destruction of political culture in the US under the Trump regime. Not that it was so much better before (it was different though), but never was the level of ugliness, really an oath of manifestation of the political hygiene, so devastatingly visible than under Trump. Us comrades in sustainability have never thought we’d see the Grim Reaper of climate change arising from the ashes of old ideology so drastically and so quickly. It is as if we’re living in one of the worst nightmares since Trumplethinskin declared that the US would step out of the Paris Climate Treaty, a massive success story of the nations of this world, hard fought for for many years. The Paris Climate Treaty, as we all know is just the basis of more that needs to happen, not the end goal of global climate management.

Even more devastating is it to witness and being dragged into the endless and useless discussions between ‘the Dems’ and ‘the Reps’ fanatics. If you follow discussions on the US news channels or on social media it leaves you speechless, it’s purely one big war out there. Every aim to seriously discuss an issue is deteriorating within minutes into an ideological fight of left against right, of liberals against the GOP, and easy for the right-wing movement to position themselves as the new gods of unity, declaring America first, even from the balconies of the White House. My stomach regularly rebels listening to all that stupidity.

There are clearly patterns in such discussions that I took part in this year. It always goes like this:

- Somebody offers a totally unsubstantiated opinion (Islamics are terrorists, the UN gets way too much money from the US, carrying guns safes lives, climate change doesn’t exist, trickle-down economics would save us, so make the rich richer, we need our (coal) jobs back, blahblah…) to justify ‘America first’.

- When asked to substantiate these opinions through facts, new and totally unrelated new opinions are thrown at you (you feel that that someone felt forced to spend 60 seconds on research, mostly digging up some wicked unsubstantiated news site).

- When revealing that the new opinions are also unsubstantiated you are called names, nut -head and idiot are some of the softest ones. And of course you are an arrogant liberal.

- When I then say that I am simply a European citizen with a decent political education, taught in political discourse, and also a German that has learnt how to detect fascist tendencies and indications of dictatorship, the answer is: so you’re even a nazi, you should shut up anyway. You have no right to exist, you should be dead.

Well, those are the moments when my family thinks I should not have started these shitty conversations at all. But then I am reminded of other people I talked to or seen in documentations that explained the slow demise of the American Midwest, the death of the steel, mining, and automobile industry, the drying out of the corn belt (also the bible belt), connected with a drying out of decent education, medication, and normal socialisation. Those that feel that the establishment in Washington has forgotten them a long time ago and that the ‘swamp needs to be dried out’. Those that suffered in the financial crises that destroyed vast parts of the American Middle Class. So yes, there are reasons that started with Reagan in the 80’s that are now exploding under Trump and produce cracks in society, even within and cutting through families. Yes, I understand all that, and many more reasons to be annoyed about the political class. So I should be more humble and better understand where these people come from.

But then I again shiver when I the see how this president shamelessly misleads these American people while his voters flee into their ideologies that produce all that bullshit as exemplified above. They, who applaud more the more foul-mouthed the flash bangs out of Trump’s Office are, how on Earth can they ever return to a minimal decency and humbleness in political culture?

I am at the point where I think that the current generation of Trump lemmings actually are ‘the lost generation’; vulgar, dangerously gun-loving, and brain-washed. Totally hopeless. And I feel sad for them. As a German one is very uncomfortable to think someone like Trump can still continue his bedevilled manipulation game, and that only the 2018 mid-elections will be bringing salvation. Or one has to wait for special investigator Mueller to release the big bang proof of Russian conspiration. Not even to think of how much more damage is possible in foreign policy, although (apart from North Korea and the Middle East) the world has more or less turned to a ‘World against Trump’ pattern there. The US is more or less alone in foreign context. A laughing stock, just with too much military budget, so one has to take every fart coming out of the White House seriously.

I am also at the point where I think the ‘organised resistance’ that started to become active everywhere in the US after the Trump disaster is a failure for the short-term ‘Trump must go – NOW’ action. Hundreds of thousands on the streets – oh that’s fake news anyway. Demonstrations – yeah they happen all the time and achieve nothing. Maybe in the beginning, but where are they now? Unfairest of all tax bills – hello, where are you guys?

What does all of that leave me with? Education, education, education. A new generation that learns about the other side – renewable energy, innovative social entrepreneurship, working at Benefit Corporations, doing project work in the circular, sharing and collaborative economy, reinforced quality in the education, medical and social sector. Continuing to individually decompose all unsubstantiated factless opinions, but also turn around and go when necessary. Believing in local change in cities and more and more states in the US that say ‘we’re still in (the Paris Climate Treaty)’, this is where most positive impact needs to happen anyway. This is where I also see the benefit and need of a longer-term ‘purpose-driven resistance movement’. Erase the two party system, a cancer in the existing political landscape, so learn from the hygiene a 4-5 party system that is dependent on coalition-building can produce. Reestablish views that ‘the other side’ isn’t the enemy, but a partner for nurturing good discussions that lead to accepted policy-making. And for me? I will continue to work dayin-dayout to make a Green, Inclusive and Open Economy a reality. That’s why I started Reporting 3.0. This is why I will relentlessly continue on that path. Until it’s there. Until the bullshit is over.

Happy winter solstice to all of my American friends. We’re in this together, and we’ll continue to be positive mavericks.

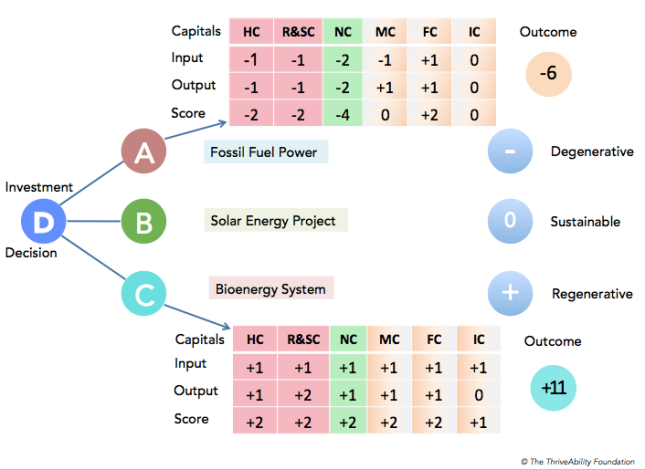

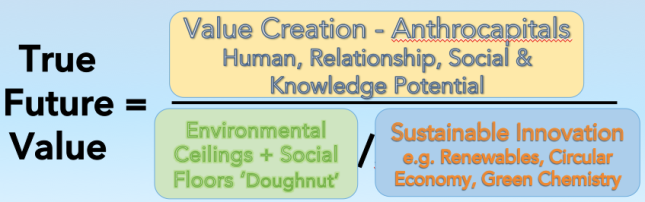

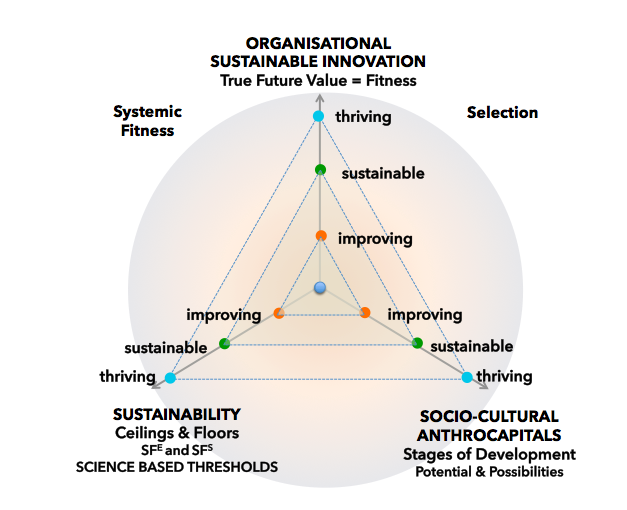

Diagram 6: High-level formula for deriving at ‘True Future Value’; a more detailed version with all variables can be sent by the author on request.

Diagram 6: High-level formula for deriving at ‘True Future Value’; a more detailed version with all variables can be sent by the author on request.

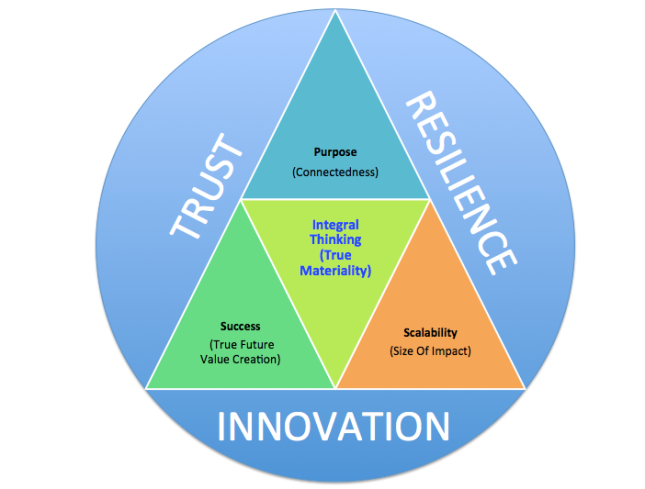

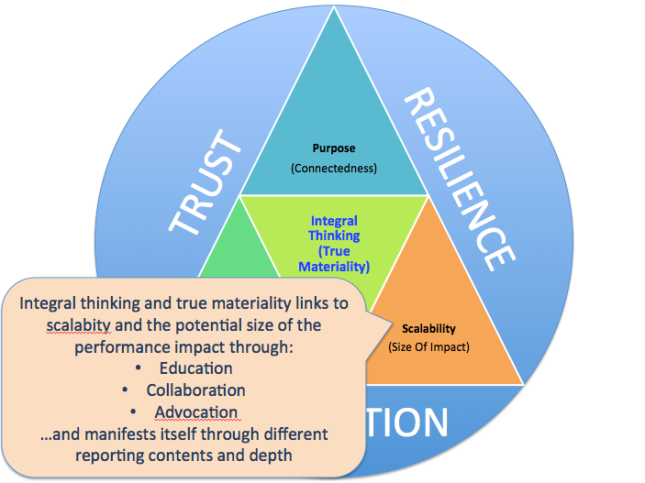

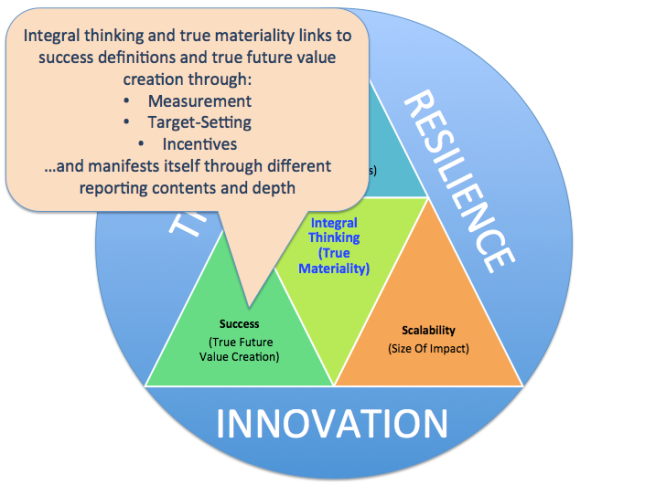

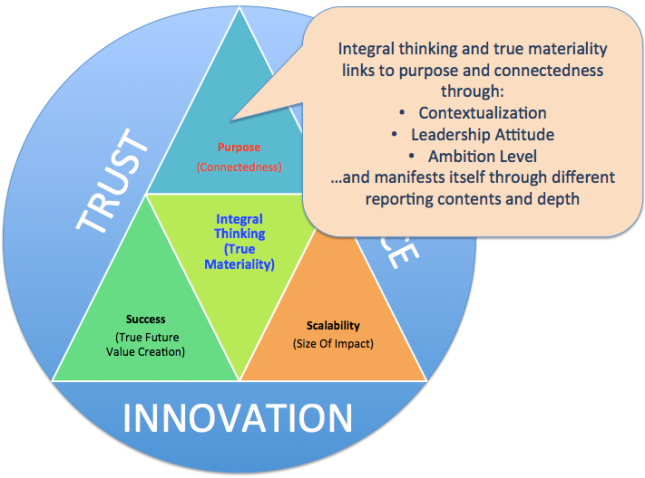

Diagram 3: Integral thinking and true materiality need a renewed focus on the purpose of the organization and connectedness to the economy we want to live in.

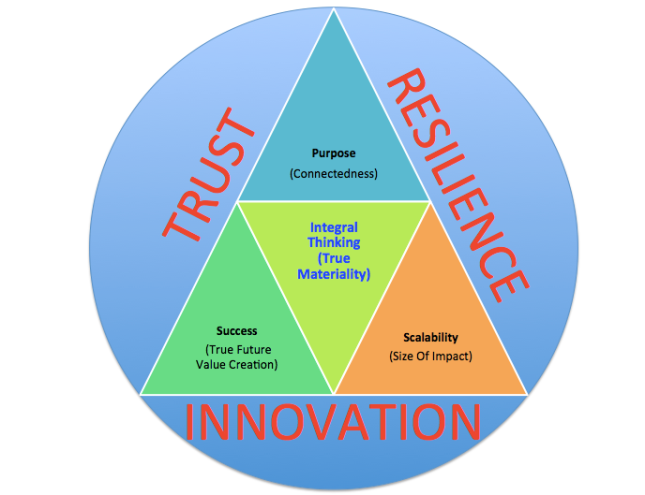

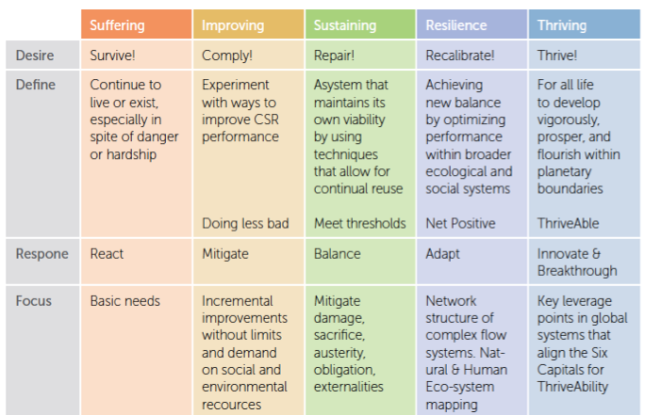

Diagram 3: Integral thinking and true materiality need a renewed focus on the purpose of the organization and connectedness to the economy we want to live in. Diagram 4: The strategy continuum to assess a company’s position in a world that needs to leapfrog from surviving to thriving (Source: A Leader’s Guide to ThriveAbility, page 18).

Diagram 4: The strategy continuum to assess a company’s position in a world that needs to leapfrog from surviving to thriving (Source: A Leader’s Guide to ThriveAbility, page 18).